The clouds are starting to half. The world economic system begins the ultimate descent towards a comfortable touchdown, with inflation declining steadily and development holding up. But the tempo of growth stays gradual, and turbulence could lie forward.

Global exercise proved resilient within the second half of final yr, as demand and provide elements supported main economies. On the demand aspect, stronger non-public and authorities spending sustained exercise, regardless of tight financial situations. On the provision aspect, elevated labor drive participation, mended provide chains and cheaper power and commodity costs helped, regardless of renewed geopolitical uncertainties.

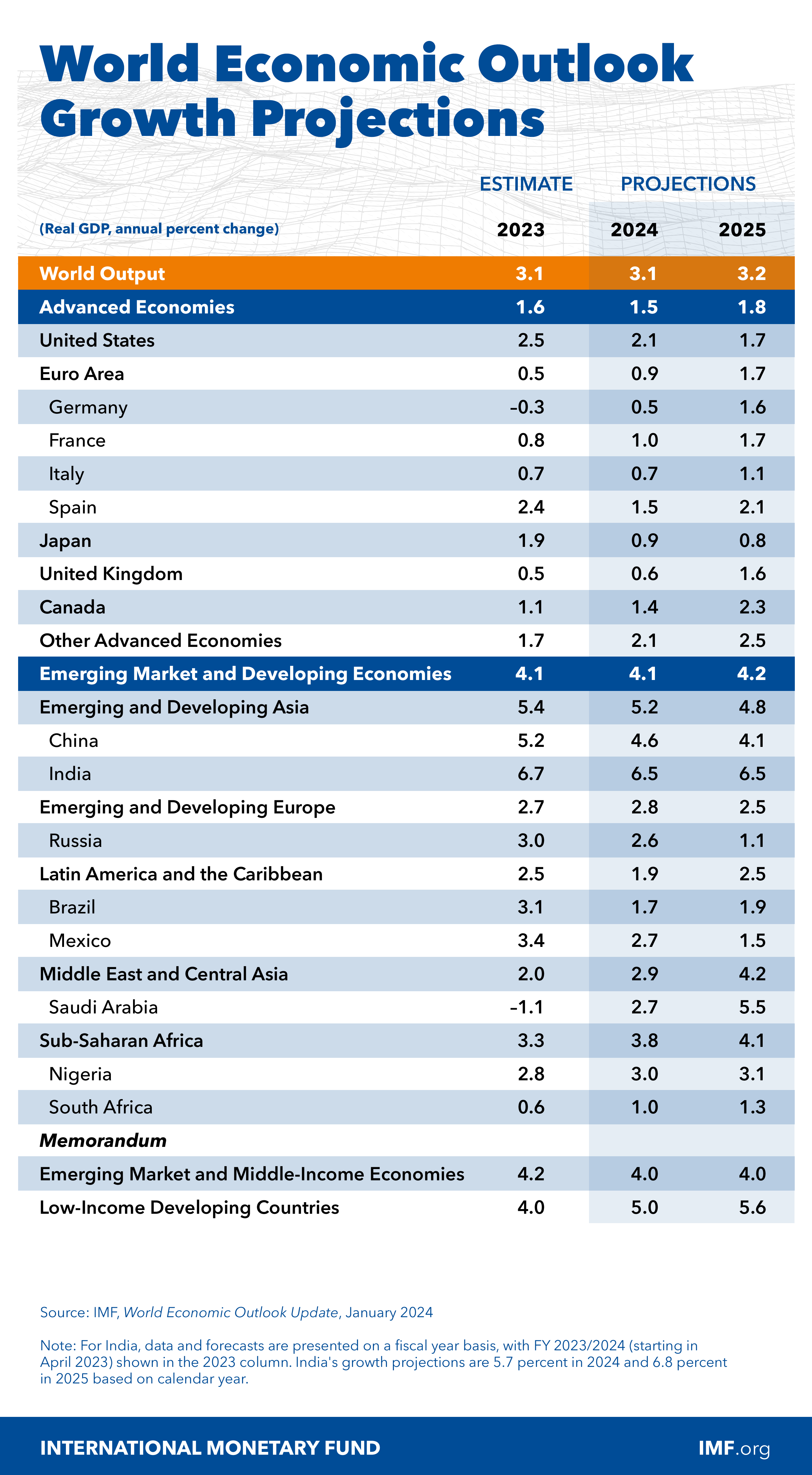

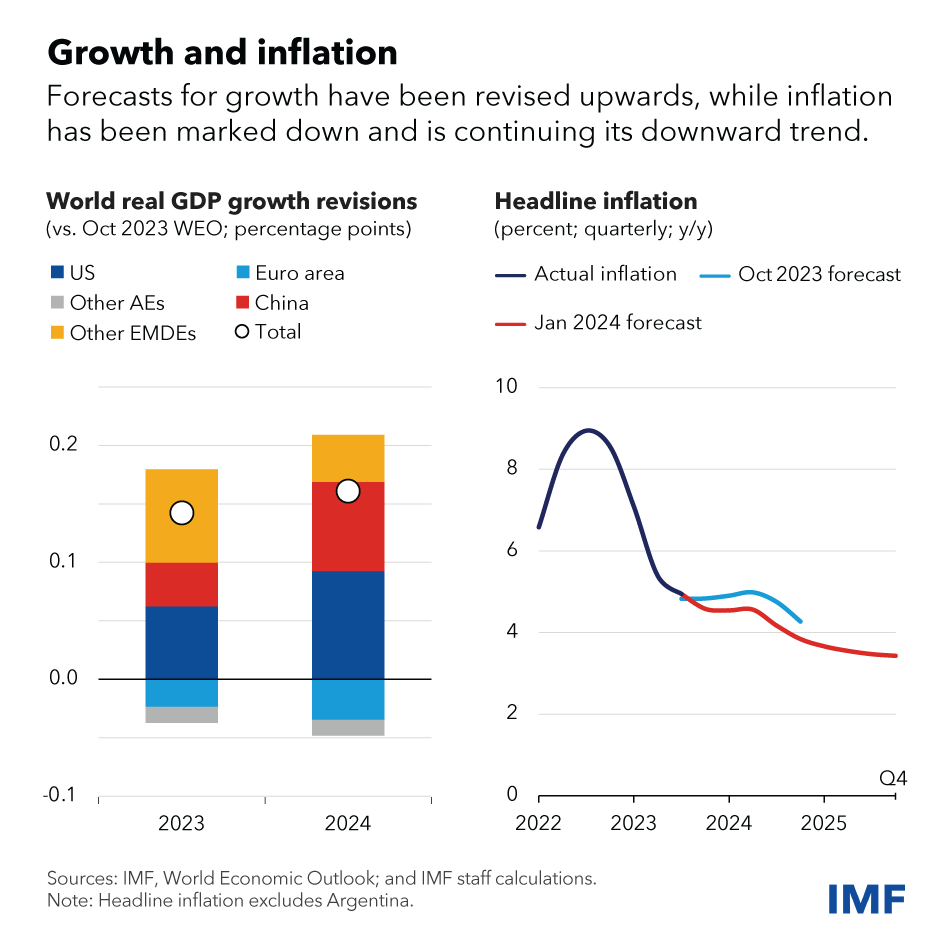

This resilience will carry over. Global growth below our baseline forecast will regular at 3.1 p.c this yr, a 0.2 share level improve from our October projections, earlier than edging as much as 3.2 p.c subsequent yr.

Important divergences stay. We anticipate slower development within the United States, the place tight financial coverage continues to be working by the economic system, and in China, the place weaker consumption and funding proceed to weigh on exercise. In the euro space, in the meantime, exercise is anticipated to rebound barely after a difficult 2023, when excessive power costs and tight financial coverage restricted demand. Many different economies proceed to point out nice resilience, with development accelerating in Brazil, India, and Southeast Asia’s main economies.

Inflation continues to ease. Excluding Argentina, world headline inflation will decline to 4.9 p.c this yr, down 0.4 share level from our October projection (additionally excluding Argentina). Core inflation, excluding risky meals and power costs, can also be trending decrease. For superior economies, headline and core inflation will common round 2.6 p.c this yr, near central banks’ inflation targets.

With the improved outlook, dangers have moderated and are balanced. On the upside:

- Disinflation might occur quicker than anticipated, particularly if labor market tightness eases additional and short-term inflation expectations proceed to say no, permitting central banks to ease sooner.

- Fiscal consolidation measures that governments have introduced for 2024-25 could also be delayed as many international locations face rising requires elevated public spending in what’s the largest world election yr in historical past. This might increase financial exercise, but in addition spur inflation and improve the prospect of disruption later.

- Looking additional forward, speedy enchancment in Artificial Intelligence might increase funding and spur speedy productiveness development, albeit one with significant challenges for workers.

On the draw back:

- New commodity and provide disruptions might happen, following renewed geopolitical tensions, particularly within the Middle East. Shipping prices between Asia and Europe have elevated markedly, as Red Sea assaults reroute cargoes round Africa. While disruptions stay restricted thus far, the scenario stays risky.

- Core inflation might show extra persistent. The value of products stays traditionally elevated relative to that of providers. The adjustment might take the type of extra persistent providers—and total—inflation. Wage developments, significantly within the euro space, the place negotiated wages are nonetheless on the rise, might add to cost pressures.

- Markets seem excessively optimistic in regards to the prospects for early price cuts. Should traders re-assess their view, long-term rates of interest would improve, placing renewed stress on governments to implement extra speedy fiscal consolidation that might weigh on financial development.

Policy challenges

With inflation receding and development remaining regular, it’s now time to take inventory and look forward. Our analysis exhibits {that a} substantial share of current disinflation occurred by way of a decline in commodity and power costs, slightly than by a contraction of financial exercise.

Since financial tightening sometimes works by miserable financial exercise, a related query is what function, if any, has financial coverage performed? The reply is that it labored by two extra channels. First, the speedy tempo of tightening helped persuade folks and corporations that top inflation wouldn’t be allowed to take maintain. This prevented inflation expectations from persistently rising, helped dampen wage development, and lowered the danger of a wage-price spiral. Second, the unusually synchronized nature of the tightening lowered world power demand, immediately decreasing headline inflation.

But uncertainties stay and central banks now face two-sided dangers. They should keep away from untimely easing that may undo many hard-earned credibility good points and result in a rebound in inflation. But indicators of pressure are rising in curiosity rate-sensitive sectors, equivalent to building, and mortgage exercise has declined markedly. It shall be equally essential to pivot towards financial normalization in time, as a number of rising markets the place inflation is properly on the way in which down have began doing so already. Not doing so would jeopardize development and danger inflation falling beneath goal.

My sense is that the United States, the place inflation seems extra demand-driven, must concentrate on dangers within the first class, whereas the euro space, the place the surge in power costs has performed a disproportionate function, must handle extra the second danger. In each instances, staying on the trail towards a comfortable touchdown will not be straightforward.

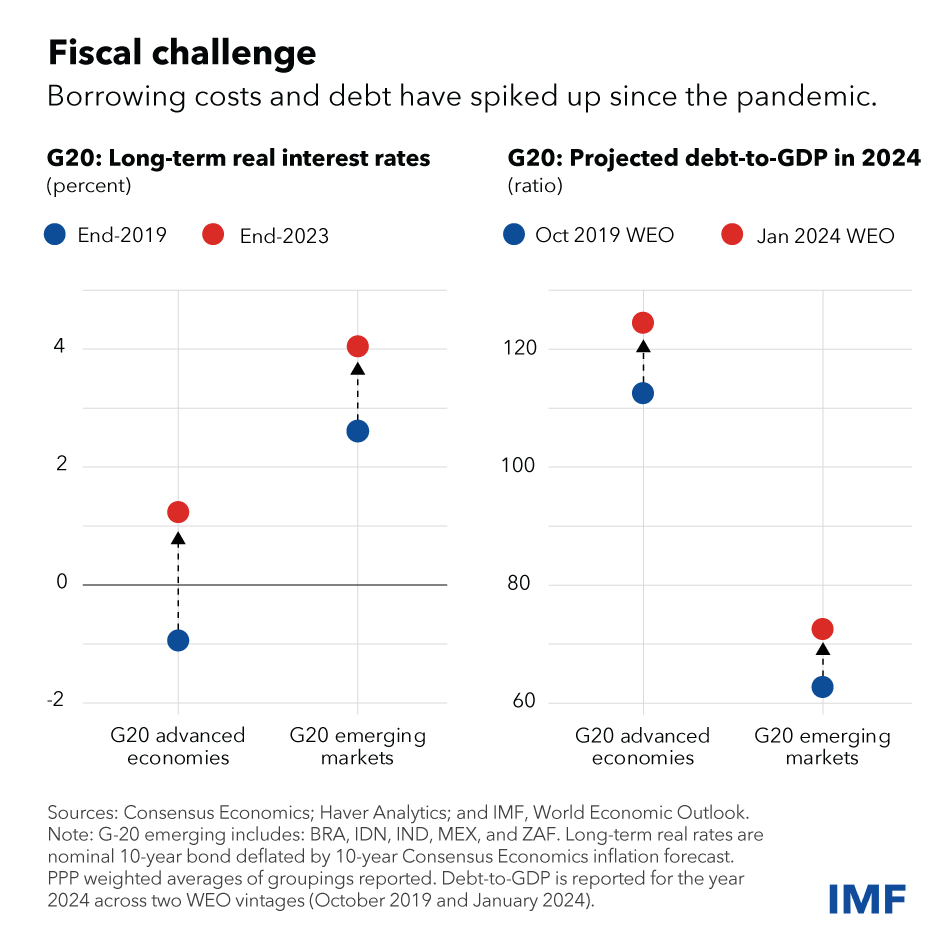

The largest problem forward of us is to sort out elevated fiscal dangers. Most international locations got here out of the pandemic and power disaster with larger public debt ranges and borrowing prices. Bringing down public debt and deficits will give house to cope with future shocks.

Remaining fiscal measures launched to offset excessive power costs ought to be phased out immediately, because the power disaster is behind us. But extra is required. The hazard is two-fold. The most urgent danger is that international locations do too little. Fiscal fragilities will construct up till the danger of a fiscal disaster forces sudden and disruptive changes, at nice value. The different danger, already related for some international locations, is to do an excessive amount of, too quickly, within the hope of convincing markets of ones’ fiscal rectitude. This might endanger development prospects. It would additionally make it a lot more durable to deal with imminent fiscal challenges such because the local weather transition.

What to do then? The reply is to implement a gentle fiscal consolidation, with a non-trivial first installment. Promises of future adjustment alone is not going to do. This first installment ought to be mixed with an improved and well-enforced fiscal framework, so future consolidation efforts are each sizable and credible. As financial coverage begins to ease and development resumes, it ought to change into simpler to do extra. The alternative shouldn’t be wasted.

Emerging markets have been very resilient, with stronger-than-expected development and steady exterior balances, partly because of improved financial and monetary frameworks. Yet divergence in coverage between international locations could spur capital outflows and foreign money volatility. This requires stronger buffers, in keeping with our Integrated Policy Framework.

Beyond fiscal consolidation, the main target ought to return to medium-term development. We mission world development of three.2 p.c subsequent yr, nonetheless properly beneath the historic common. A quicker tempo is required to deal with the world’s many structural challenges: the local weather transition, sustainable improvement, and elevating dwelling requirements.

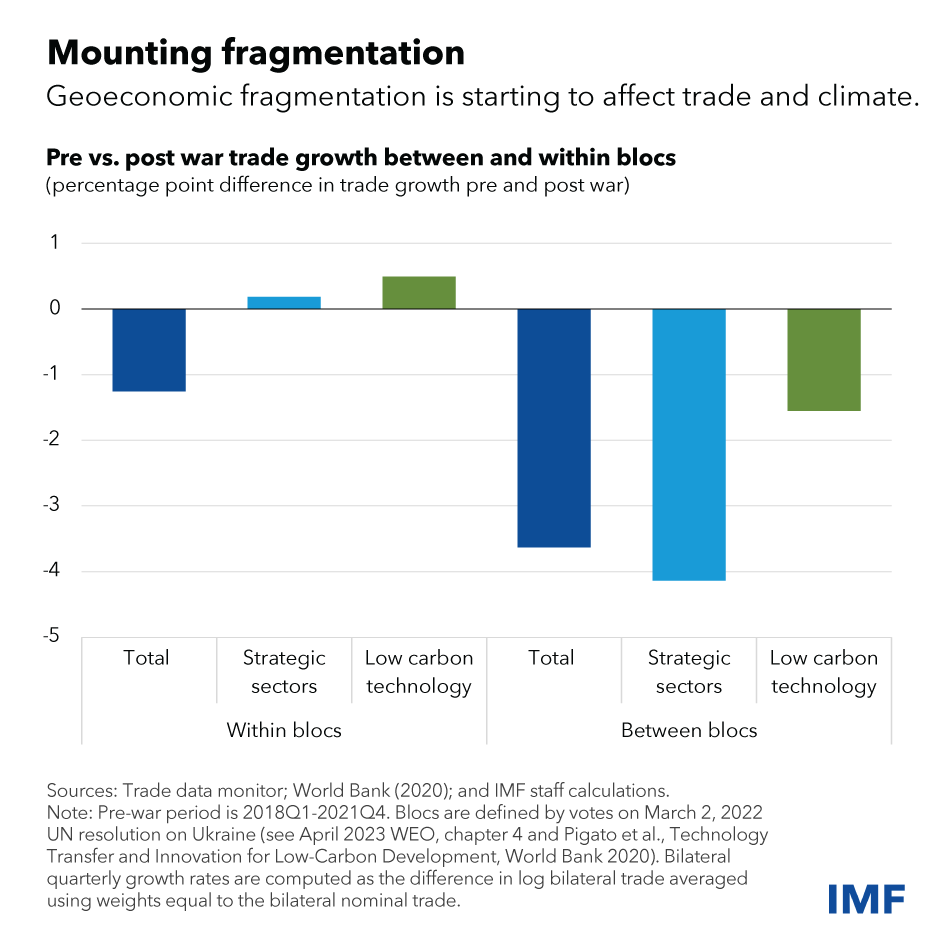

Reforms that ease probably the most binding constraints to financial exercise, equivalent to governance, enterprise regulation and exterior sector reform, may help unleash latent productiveness good points, our research shows. Stronger development might additionally come from limiting geoeconomic fragmentation by, for example, eradicating the commerce limitations which are impeding commerce flows between completely different geopolitical blocs, together with in low-carbon expertise merchandise which are crucially wanted by rising and growing international locations.

Instead, we must always attempt to maintain our economies extra interconnected. Only by doing so can we work collectively on shared priorities. Multilateral cooperation stays one of the best strategy to deal with world challenges. Progress towards that, such because the current 50 percent increase of the Fund’s everlasting sources, is welcome.